The Michigan Launch Initiative: The Road Traveled Too Often

Stadium, spaceport, and monorail proposals have a few things in common. Unfortunately, one significant commonality relies on twisting facts and supplying doses of unrealistic optimism.

An Homage to Lyle Lanley

“I think everybody turned around, like we did, and said, ‘What did we win?’”

The above question references spaceport studies and efforts that are a part of the Michigan Launch Initiative (MLI). It’s from a space financing company’s CEO, Donald Moore. The reasons why MLI was initially considered were answered in a presentation promoting its adoption:

“Networked constellations of LEO satellites are being planned. 12,000 are planned for the next decade (versus 1,200 satellites currently in LEO). Existing launch facilities are insufficient to meet launch demand. Multibillion impact on Michigan’s economy.”

In other words, companies are planning to deploy many satellites, and Michigan needs to get a part of that.

The presentation containing that rationale is…interesting.

Moore asks the kind of question people usually ask when it’s already too late. It’s asked when a spaceport initiative takes on a life of its own, sucking county, state, and federal taxpayer money down a feeding tube facilitated with opaque decisions and/or litigation. The result doesn’t seem to benefit the locals, no matter what promises were pitched. Spaceport pitches are an old subset of an older plethora of cautionary tales involving projects promoting malls, stadiums, and monorails.

The Simpson’s fans might understand the spaceport scenario better using a monorail context. In one particular episode, a slick salesman, Lyle Lanley, pitches Springfield on the idea of needing a monorail. Unlike real-life and most current spaceport efforts, Springfield built the monorail quickly, which then failed spectacularly. But, like Springfield’s citizens’ initial reaction to the monorail, it’s easy for real people to get excited about the idea of a spaceport. It sounds very futuristic. It initially excited the imaginations of the citizens living in New Mexico, Georgia, Florida, and other states and communities. After all, surely such high-technology facilities require workers (hopefully local), which might increase taxes collected, help with school and infrastructure projects, etc.

Ultimately, while the instigators for these spaceport proposals aren’t necessarily startup ventures, they appear to similarly rely on one of the three F’s for getting funding (as discussed before): family, friends, or fools. Additionally, the spaceport idea (and its many possible positive incentives) tamps down any less-foolish person’s attempt to inject common sense into spaceport go/no-go discussions. The combination appears to work because ventures that should never have been considered begin a seemingly endless cycle while somehow maintaining funding from the same foolish source.

There are several reasons why people initially get cajoled into accepting the possibility of a spaceport in their community. First, as noted earlier, the perceived benefits of a nearby spaceport are tempting. Perhaps another reason is they may have a different idea of what a spaceport is. For them, a spaceport is Kennedy Space Center or Flash Gordon. It’s the vibrant future. But that is not how others, such as the Federal Aviation Administration (FAA), define what a spaceport is.

The Naming of Spaceports is a Difficult Matter

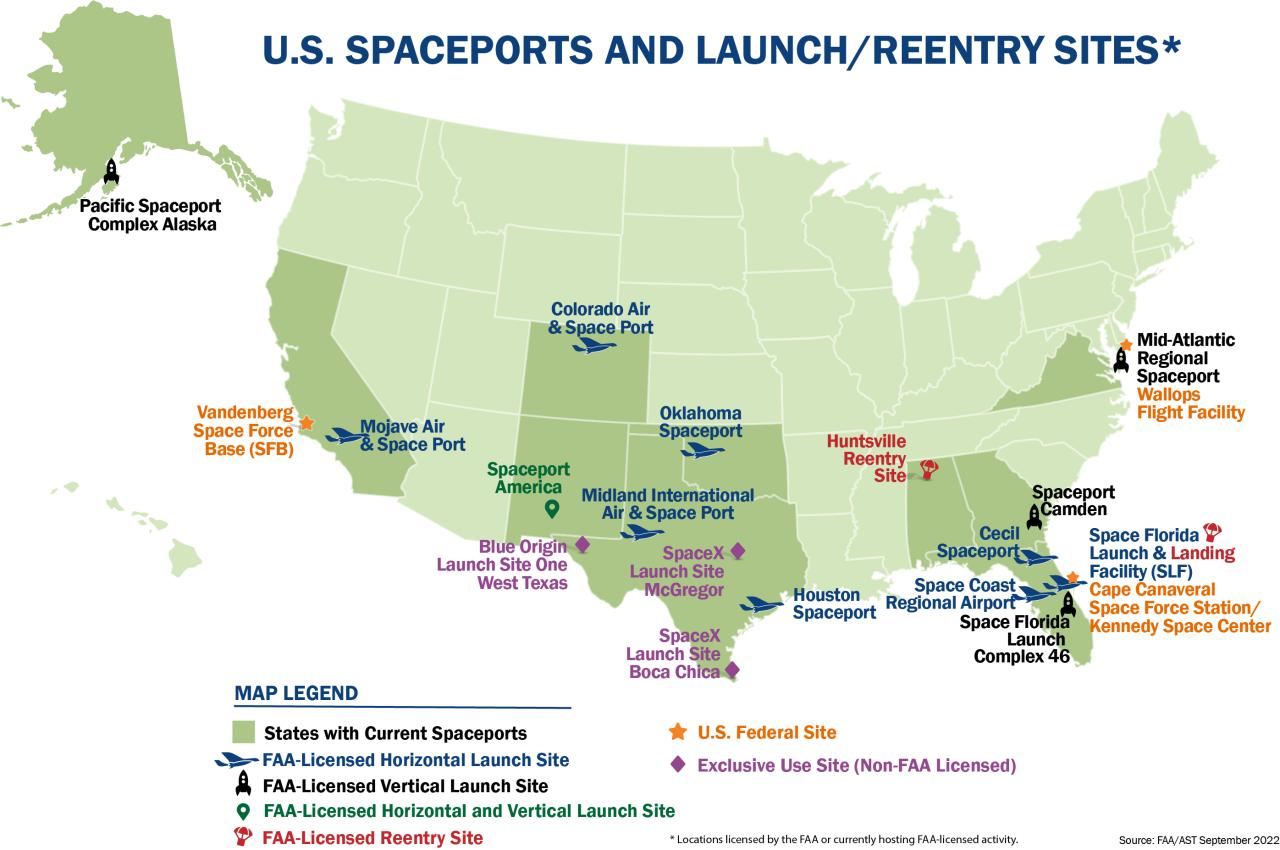

The FAA has given 21 licenses to various U.S. commercial “spaceports.” But are they all spaceports? The FAA’s accounting is curious, as according to the Center for Strategic and International Studies (CSIS), there are 22 active spaceports globally. I tend to view the CSIS definition as the more honest view of a spaceport. It defines the spaceport “as a ground-based launch facility that has been used for at least one successful orbital launch.” It also notes that the word active “describes spaceports that have both supported at least one orbital space launch over the past 10 years and have not been declared inactive by its operator.”

Surely, the FAA has a nice, succinct definition of a spaceport. After all, it has one for airport: “…an area of land or water that is used or intended to be used for the landing and takeoff of aircraft, and includes its buildings and facilities, if any.” However, by contrast, the FAA does not define a spaceport. Instead, it focuses on launch and reentry sites and uses those terms' definitions as the basis for a spaceport. I won’t make this analysis a list of definitions, but the FAA’s launch site fails to make a distinction between orbital and suborbital launches.

It also doesn’t indicate whether any of its current spaceport license-holders are actively launching anything. It’s unclear what active means to the FAA, as a December 2021 graphic labels them “actively private.” That changed in the latest September 2022 graphic, showing how the agency still muddles definitions. The problem with that muddling is that the FAA’s data is accepted as more “official” than other data, including the map CSIS published.

{kind=link}

That muddling makes the U.S. space launch industry appear more dynamic than it is–with the Federal government seeming to bless that interpretation. That appearance of assurance is a problem for those unfamiliar with the industry and is why some analysts see the use of FAA space data as cause for concern. Even drilling down through the FAA’s site demonstrates how its muddled data can be misconstrued. Remember, the launch industry appears busy because there are 21 spaceports with licenses–that’s because the FAA lists those launches under the title “Spaceports by State.”

However, eight of those listed licenses are generally consolidated between three major U.S. orbital launch areas (spaceports) at Kennedy Space Center (Florida), Vandenberg Space Force Base (California), and Wallops Island (Virginia). Of the remaining 13 licensed spaceports, only one other site, the Pacific Spaceport Complex (PSC-Alaska), is used for orbital launches. In addition, four of the unaccounted 12 spaceports have managed to conduct suborbital launches: Blue Origin’s Launch Site One; SpaceX’s Boca Chica; Spaceport America; and Mojave Air and Space Port. That leaves eight licensed U.S. “spaceports,” none of which have launched orbital or suborbital rockets for the last decade.

More Launch Capacity Needed?

Again, that kind of accounting flexibility, lack of definitions (ill-defined, perhaps?), and activity criteria make it seem to the uninformed that the U.S. space industry is much more active than it is. This may be why the MLI “Why” statement included the assertion that more orbital launch sites are required. But that assertion isn’t accurate.

In an extremely active year of launches, such as 2021, the world’s launch companies/agencies attempted to launch 146 orbital rockets (135 were successful). Forty-five were launched from the four U.S. launch spaceports(Kennedy/CCSF, Wallops/MARS, Vandenberg, PSC). If we were to divide those launches by four (the number of orbital U.S. spaceports), that would come out to ~11 launches per spaceport. But that spread didn’t happen. Of those orbital U.S. launch attempts, 31 occurred from space launch complexes at Kennedy Space Center and Cape Canaveral Space Force station. The remaining 14 were divided among the other three, with seven going to Vandenberg.

That doesn’t sound like there are insufficient orbital spaceports. True, two existing spaceports launched more rockets but they didn’t reach maximum launch capacity (based on this year’s SpaceX activity). The other two, however, averaged much less than a launch every two months. Worse for the MLI project, PSC has a more advantageous geographic location for polar orbit smallsat launches than Michigan (highlighted in the MLI presentation). Yet, despite that stellar advantage, it is less busy than Rocket Lab’s New Zealand spaceport.

U.S. suborbital launch activity from Launch Site One (6) and Spaceport America (2) during 2021 is also very spare. Blue Origin hasn’t provided plans for launching New Shepard rides anywhere other than its Texas site. Virgin Galactic has mentioned the intent to turn its fair ride into suborbital transportation eventually–but it’s launched SpaceShipTwo less often than Blue Origin has launched New Shepard. So again, neither company’s launch pace demonstrates a need for another spaceport.

Even future orbital U.S. launch vehicles, whether Vulcan, New Glenn, or Starship, will not be launching too far from current company launch complexes. That is important because each is involved in plans to deploy the thousands of LEO satellites MLI mentions as the rationale for building a Michigan spaceport. It’s doubtful Blue Origin, SpaceX, or United Launch Alliance will be tempted to build launch infrastructure in Michigan. But perhaps one should never underestimate the power of government subsidies.

It all adds up to Michigan becoming yet another state with a spaceport to nowhere. In the article I referenced at the beginning of this analysis, the author mentions a research institute report that questioned MLI’s plans. The report's author noted that the business assumptions for MLI’s spaceport don’t make a business case. The author was convinced that the additional annual revenues from a spaceport would equal those of two fast food restaurants. It would be good for the local Michigan governments to heed that observation while learning lessons from spaceports in other states. Or from The Simpsons.

It seems like every state (and city) thinks they need a launch site to be part of the NewSpace race, likely because it's so visible and high-profile. Any examples of states or cities out there jumping into STEM and NewSpace promotion by more reasonably - and with less risk - working to bring in or help start up companies building sats, components, software or other capabilities with tax incentives and other lures?